|

Getting your Trinity Audio player ready...

|

The financial services industry is undergoing one of the most profound transformations in modern history. A few years ago, opening a bank account, applying for a loan, or buying insurance required visits to physical branches and lengthy paperwork. Today, thanks to Embedded Finance and Banking-as-a-Service (BaaS), financial products are available instantly—often inside apps that aren’t even banks.

Think about it: you book a ride on an app and pay seamlessly without leaving the platform, you shop online and get instant credit at checkout, or you buy a phone and add insurance in just two clicks. None of these experiences require direct interaction with a traditional financial institution. This seamless integration is what embedded finance and BaaS are all about.

Industry experts estimate that the embedded finance market could reach $150 billion globally by 2025, reshaping payments, lending, insurance, and investments for both businesses and consumers.

What Is Embedded Finance?

Embedded finance is the integration of financial services into non-financial platforms. Instead of customers visiting a bank or financial institution, financial tools are “embedded” within the everyday apps and platforms they already use.

- Examples of Embedded Finance:

- E-commerce: Buy-now-pay-later (BNPL) at checkout.

- Ride-hailing apps: Digital wallets, instant payments, or micro-loans for drivers.

- Social media platforms: Peer-to-peer payments or tipping creators.

- Travel booking sites: Integrated travel insurance when buying tickets.

By reducing friction, embedded finance enhances customer experience and creates new revenue streams for businesses.

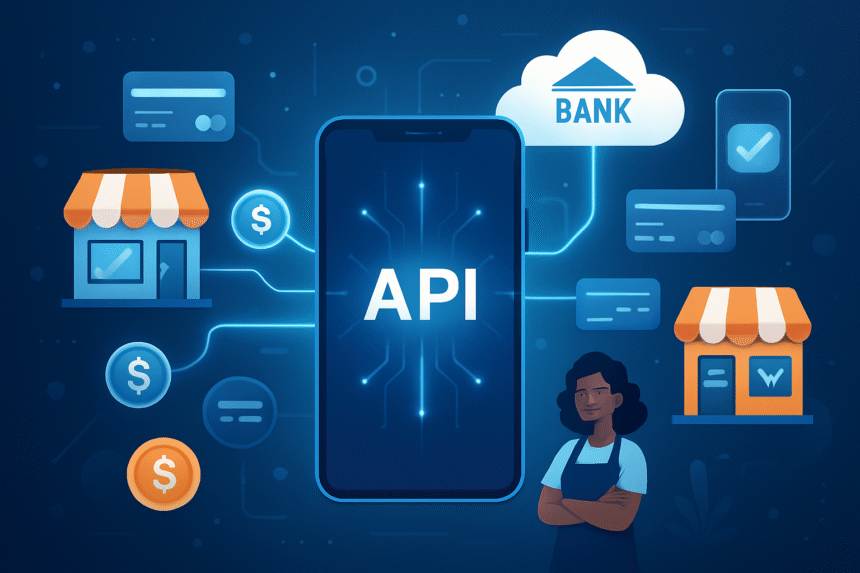

Understanding Banking-as-a-Service (BaaS)

While embedded finance is what users see, Banking-as-a-Service is the backbone that makes it possible. BaaS platforms provide APIs (application programming interfaces) that allow non-financial companies to connect with licensed banks and offer financial products.

- How BaaS Works:

- A licensed bank provides core financial infrastructure.

- A fintech or technology provider creates a BaaS platform with APIs.

- A non-financial business integrates these APIs to embed financial services.

For example, an online retailer doesn’t need to become a bank to offer credit. Instead, it plugs into a BaaS provider’s API, which connects to a licensed bank that issues the credit.

Why Embedded Finance and BaaS Are Booming

Several factors are driving this revolution:

- Customer Expectations: Today’s consumers expect convenience and speed. They prefer financial services to be part of their existing digital journeys rather than standalone interactions.

- Digital Transformation: Businesses across industries are digitizing operations, making it easier to integrate financial services.

- New Revenue Opportunities: By embedding payments, loans, or insurance, companies add extra income streams.

- Open Banking Regulations: Policies in many countries are encouraging innovation and secure sharing of financial data, which fuels BaaS adoption.

- Rise of Fintech Infrastructure Players: Companies like Stripe, Plaid, Marqeta, and Railsr have simplified integration, accelerating the growth of embedded finance.

Key Use Cases of Embedded Finance

1. Payments Integration

The most common example is integrated payments. Customers can pay for services without switching apps or entering card details repeatedly.

- Uber, Ola, and Lyft offer embedded wallets.

- Amazon and Flipkart provide one-click checkout with saved cards.

2. Lending & Buy Now, Pay Later (BNPL)

BNPL services such as Klarna, Affirm, and Afterpay let customers split payments into installments at checkout, increasing sales and affordability.

3. Insurance at Checkout

When booking flights, platforms like MakeMyTrip or Expedia offer instant travel insurance. Similarly, electronics retailers embed device insurance.

4. Wealth Management & Investments

Apps are embedding robo-advisors and micro-investment options. For example, Paytm in India offers mutual funds and digital gold inside its app.

5. Payroll & Employee Benefits

HR tech platforms now embed financial services like salary advances, investment options, and health insurance for employees.

Global Market Potential

The embedded finance market is projected to hit $150 billion by 2025, and some reports suggest it could reach $7 trillion by 2030 when accounting for the broader ecosystem.

- North America & Europe: Leading in BNPL and payments innovation.

- Asia-Pacific: Massive adoption in e-wallets and super apps like Grab, Gojek, and Paytm.

- Africa: Fintech startups embedding micro-lending and mobile money services in everyday platforms.

Benefits for Stakeholders

For Consumers:

- Seamless experiences

- Faster access to credit and insurance

- Fewer steps in checkout or onboarding

For Businesses:

- Increased customer loyalty and engagement

- Higher conversion rates in e-commerce

- New revenue streams from financial services

For Financial Institutions:

- Extended reach via partnerships

- New ways to monetize APIs and infrastructure

- Faster customer acquisition at lower costs

Challenges and Risks

Despite the promise, embedded finance and BaaS also face hurdles:

- Regulatory Compliance: Non-financial companies offering financial services must still comply with banking regulations.

- Cybersecurity Risks: Handling financial data increases exposure to cyber threats.

- Customer Trust: Users must trust that embedded financial services are secure and reliable.

- Over-Reliance on Tech Providers: Businesses depend heavily on BaaS providers for uptime and compliance.

The Future of Embedded Finance & BaaS

Looking ahead, several trends stand out:

- Deeper Personalization: AI will tailor loans, insurance, and investment offers in real-time based on customer behavior.

- Cross-Border Finance: Embedded solutions will simplify international payments and remittances.

- Sustainability: Green finance products, like carbon tracking and eco-friendly loans, will be embedded into consumer platforms.

- Wider Adoption by SMEs: Small businesses will adopt embedded finance to compete with larger players.

By 2030, experts predict that embedded finance will no longer be a trend but a standard expectation across industries.

Conclusion

Embedded finance and Banking-as-a-Service represent a $150 billion revolution that is reshaping how we interact with money. From payments to lending, insurance, and investments, financial services are no longer confined to banks—they’re becoming invisible, seamlessly integrated into the apps and platforms we already use every day.

For consumers, it means faster, simpler, and more convenient access to financial tools. For businesses, it unlocks new revenue opportunities and customer loyalty. And for the fintech ecosystem, it signals the beginning of a new era of innovation.

As regulations evolve and technology matures, embedded finance is set to become the backbone of digital economies worldwide—transforming not just how we pay, borrow, or insure, but how we live and interact in the digital age.

About the Author

Beyond his commitment to technology journalism, Ankit is a joyful gymgoer who believes in maintaining a balanced lifestyle.