|

Getting your Trinity Audio player ready...

|

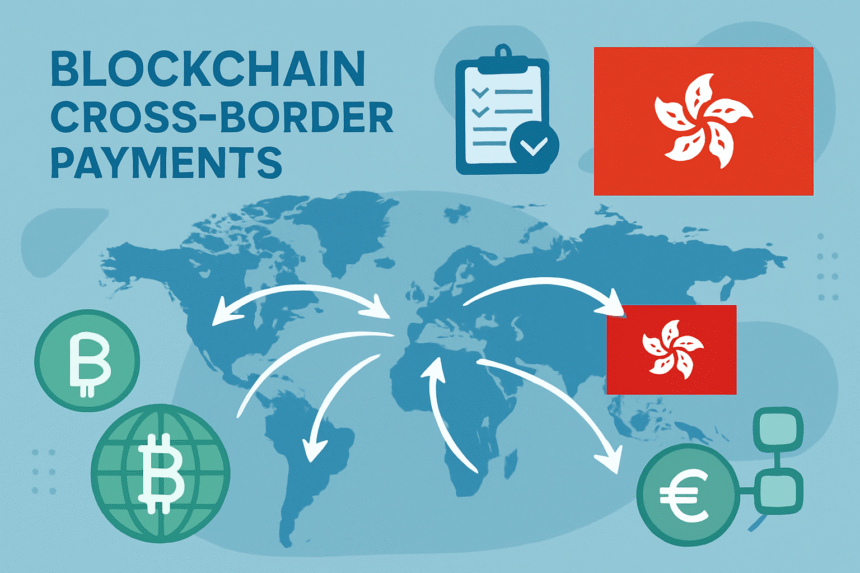

Cross-border payments have long been a pain point in global finance—slow, costly, and burdened with complex regulations. Hong Kong, however, is rapidly emerging as a global fintech hub, thanks to its clear regulatory framework and blockchain-driven infrastructure. With the Stablecoins Ordinance, the HKMA Payment Connect system, and growing private-sector investment, Hong Kong is setting the stage for seamless, real-time global transactions.

In this Article, we’ll explore how blockchain-powered cross-border payments in Hong Kong are reshaping the fintech landscape, why regulatory clarity matters, and what this means for businesses, SMEs, and consumers worldwide.

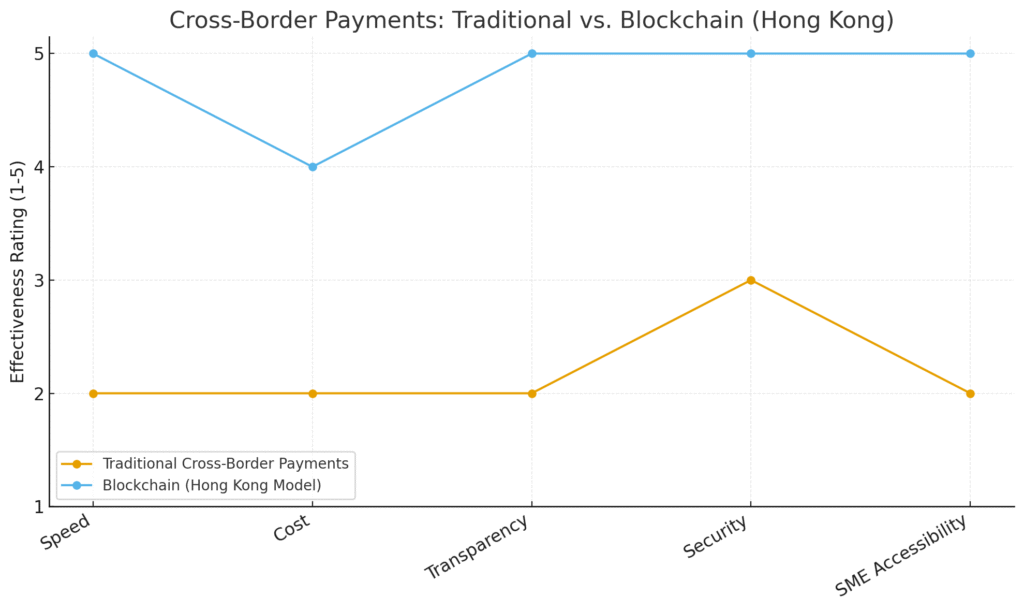

📊 Traditional Cross-Border Payments vs. Blockchain (Hong Kong Model)

Blockchain excels in speed, transparency, security, and SME accessibility compared to traditional methods.

The Cross-Border Payments Problem

Traditionally, cross-border transactions relied on correspondent banking networks. This system is:

- Expensive – Multiple intermediaries mean high fees.

- Slow – Transfers often take 2–5 days.

- Opaque – Tracking funds across borders can be difficult.

- Inefficient for SMEs – Smaller firms face delays and high transaction costs.

With globalization and e-commerce booming, the demand for instant, transparent, and cost-efficient payments is stronger than ever.

Hong Kong’s Blockchain Solution

Hong Kong has taken a bold step toward solving these challenges by leveraging blockchain technology and progressive regulation.

1. Stablecoins Ordinance

This new legislation provides legal certainty around stablecoins, ensuring they are regulated, asset-backed, and secure. By doing so, Hong Kong positions itself as a safe hub for blockchain-based settlements.

2. HKMA’s Payment Connect

The Hong Kong Monetary Authority (HKMA) has launched initiatives like Payment Connect, enabling real-time RMB/HKD cross-border settlements. This creates a more efficient financial bridge between Mainland China and international markets.

3. $2.4 Billion Fintech Investment in 2024

The regulatory clarity has attracted massive capital inflows, with $2.4B invested into Hong Kong fintech startups in 2024. Much of this funding is flowing into blockchain, payment infrastructure, and digital assets.

Benefits of Blockchain-Based Cross-Border Payments

- ⚡ Speed: Near-instant settlement compared to days in traditional banking.

- 💰 Lower Costs: Reduced reliance on intermediaries means cheaper transfers.

- 🔎 Transparency: Blockchain provides traceability, reducing fraud and disputes.

- 🌍 Financial Inclusion: SMEs and underbanked communities can access efficient payment channels.

- 🔐 Security: Cryptographic verification enhances transaction safety.

Why Regulatory Clarity Matters

While blockchain holds huge potential, its adoption depends heavily on trust and regulation. Hong Kong’s regulatory clarity has:

- Encouraged institutional adoption by banks and fintech firms.

- Attracted foreign investment into its fintech ecosystem.

- Provided a model for other financial hubs considering blockchain for payments.

Without this clarity, innovation often stalls due to legal uncertainty and compliance risks. Hong Kong’s proactive stance ensures innovation with accountability.

Global Implications

Hong Kong’s blockchain cross-border ecosystem is not just a regional development—it has global significance.

- China Integration: Strengthens RMB internationalization efforts.

- Asian Leadership: Positions Hong Kong as a leader in blockchain finance across Asia.

- Worldwide Benchmark: Offers a framework for other economies exploring blockchain payment rails.

- Crypto-Linked Banking Evolution: Stablecoins and CBDCs may soon integrate, creating hybrid payment ecosystems.

The Future of Cross-Border Payments

Looking ahead, we can expect:

- Stablecoin-Backed Trade Finance – Faster trade settlements using digital currencies.

- CBDC Integration – Linking Hong Kong’s system with China’s digital yuan (e-CNY).

- Interoperability Networks – More global payment corridors using blockchain.

- Retail Access – Businesses and individuals using blockchain payments directly in daily trade.

Conclusion

Hong Kong’s blockchain-powered cross-border payment ecosystem is proving that regulatory clarity is the real key to innovation. By combining progressive policy, investment inflows, and cutting-edge technology, the city is redefining how money moves across borders.

For fintech startups, global businesses, and everyday consumers, this marks the beginning of a new era of fast, low-cost, and transparent international transfers.

About the Author

Beyond his commitment to technology journalism, Ankit is a joyful gymgoer who believes in maintaining a balanced lifestyle.